By Barney Smith

Thursday 25 March 2021 saw the release of the sixteenth annual report by the Global World Energy Council (GWEC) . The title “Wind Energy’s role on the road to Net Zero” shows that Climate Change is back on the agenda, and the report also notes the trend for countries to announce net zero targets with major companies following suit.

Yet what is perhaps most striking about the report ( for calendar year 2020) is that, whatever the influence of COVID, total global capacity rose by some 93 Gigawatts., This represents a rise of an unprecedented 53 per cent to give a grand total of 743 GW of wind capacity installed.. The second key fact is that this increase, though very impressive, is not enough. Somewhat dauntingly, GWEC states that we will need to double the size of that increase to 180 GW every year, if we are to reach the decarbonisation and energy targets set by the Paris Agreements. Every year we fall short magnifies the target for the following year (s).

The GWEC report is the most widely used source of data on the wind energy sector for industry, governments and others. The essential message is that for the future renewables can provide an increasing share of world electricity demand provided that the enabling infrastructure is improved. For it asserts that it is the non-economic issues that are now crucial. The technology is increasingly familiar and, as unit costs fall, there is apparently plenty of investment money ready to be deployed, but swifter action on permits, on licensing and on a number of other key governance issues is vital if current progress is to be maintained..

As in 2019, China and the USA were the world’s largest onshore wind markets accounting for almost three quarters of all new capacity ,driven by the Feed in Tariff cut off in China and the scheduled phase out of the full rate Production Tax Credit in the US.

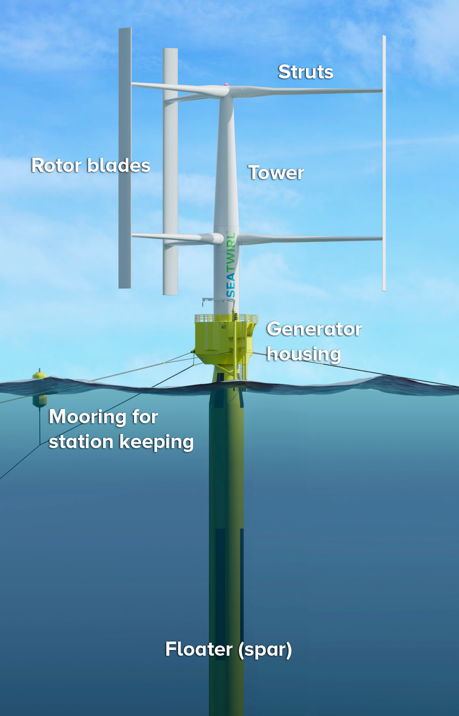

As in 2019, China installed more off-shore wind than any other country. But in this niche area the UK still remains the world leader in terms of total installed capacity. Intriguingly the listing of off-shore wind projects includes two floating platforms deployed in (or by) Portugal. This suggests that there may be future interest in adapting this technology for off-shore wind, piggy-backing on long-term experience in the Oil and Gas industry. Interestingly the British prime Minister, Boris Johnson, in talking of this technology qualified it as “Brand new” and subsequently committed to1GW of electricity being produced using this technology by 2030.

It is perhaps significant that in 2020 capex committed to off-shore wind overtook investment in off-shore oil and gas for the first time. Furthermore

the accompanying webinar echoed the report in recognising that Oil and Gas companies will need to make a rapid transition to renewable energy in order to survive and play their role in the energy transition. They have already shown greater interest than any other industry in investing in windpower. Finally, the report also suggests that emerging technological solutions such as green hydrogen and Power to X may be fertile fields for the wind industry.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}