We last wrote about AIM-listed Altona Energy on 15 August 2016. The first para of our report said that “Altona last appeared in Greenbarrel in February 2014. Since then there have been a lot of changes but little progress.”

Now a further 16 months on, the company’s audited Final Results Report for the financial year ended June 30 2017 together with a list of post- period-end developments, released in December 2016, show progress of a kind has been made. The progress has not been in the direction of travel the company has pursued for so long. But it seems likely to lead to a profitable exit strategy from the company’s existing past endeavours.

Altona hold licenses to explore the large Arckaringa coal deposits of an estimated 7,800 tonnes that lie below an uninhabited area of South Australia covering around 2,500 sq kms some 600 miles NW of Adelaide. At the time the licences were acquired in 2005 the intention was to extract coal from a conventional open cut coal mine, then process it in a Coal to Liquid (CTL) plant. Subsequent studies showed that a better economic solution was to build two plants, one for CTL and one for Coal to Methanol (CTM).

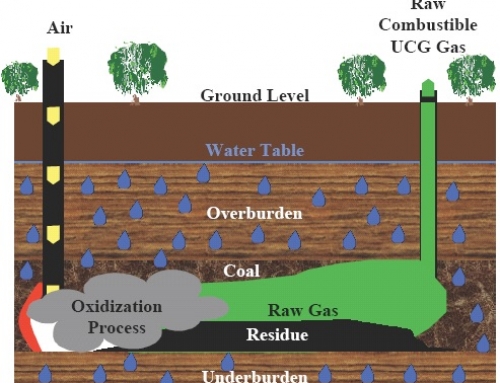

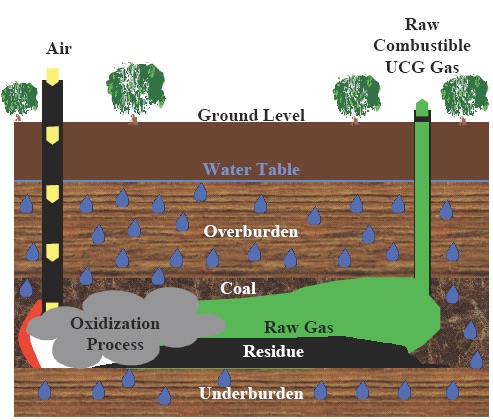

However in 2014/15 the drop in oil price and possibly the change in Australian government disrupted these plans. Costs were reduced by closing offices in Beijing and London. Above all, the objective was changed from CTL/CTM to underground coal gasification (UCG). The attraction of UCG is that most of the dirty work is done underground and the operation can be classified as clean-tech.

UCG has been tried several times in different parts of the world but has never been commercial. Altona started work on a three-year Bankable Feasibility Study for UCG. The next step was to have been to drill some exploration wells. At this point (28 July 2016) the group had been told by the South Australian government that in order to start this test drilling it needed to have a petroleum exploration licence (PEL).

Altona’s Arckaringa coal desposits are 600 miles NW of Adelaide

As it happened there was a PEL on the relevant area that overlapped the group’s Arckaringa acreage but it was owned by someone else. After much coming and going and various fruitless negotiations, Altona found that early in July 2017 it was unable to acquire the PEL 604 application. So no PEL, no UCG project. Altona postponed an issue of shares to one of the JV partners the PEL application Sino-Aus and the JV returned an initial payment of AU$5.4million.

The company’s financials were not in great shape by July 2017. The loss before taxation for financial year 2017 was £341,000 (2016: profit before tax £38m). As at June 30 2017 cash at the bank was £15,000 (2016:£362,000.) The share price in late July August 2017 was 0.38pence up from a year’s low of 0.28p but well below the high of 1.3p.

In the post-period end new management was put in place with the appointment of Nick Lyth and Phil Sutherland as Chief Executive Officer and Operations Officer respectively. Also the company raised just over £1m in four separate placings two of them priced at 0.5p a share. The company on 19 August 2017 then announced that it had settled on a new strategy of focusing on conventional coal extraction from Arckaringa. This plan was informed by the knowledge that the price for coal had more than doubled to US$ 100 a tonne in the previous 22 months and this could transform the economics of extraction.

The group engaged mining consultants WSP Australia PTY to report on the extent and economic viability of exploiting “dry” or “wet” coal in the three tenements (tenements = licences or holdings) within Arckaringa – Murloocoppie, Wintinna and Westfield. The group reported to shareholders on 25 September 2017 that this initial report had proved inconclusive, and a more focused report would be needed.

Another specialist mining consultant Runge, Pinock, Minarco Global concentrated on Westfield. It reported that a seam of between 3-6metre thickness had been confirmed, there was a groundwater level of only 10m above the seam in places and the seam had as little as 80m of coverage in places. Westfield is estimated to contain 800m tonnes coal in total.

In short this is a substantial “wet” resource ideal for open cut mining which is less costly than other methods. Nick Lyth said: “The group hopes to take advantage of high coal price, by proving up its plan in order to provide a possible exit within a reasonable time frame.

The share price of the £7.53m market cap company was 0.47p last evening, against a 52-week high of 0.54p.

{kind=link}

{kind=link}