By Julian Singer

Tees Valley Lithium (TVL) aims to build what it claims will be the first major low carbon Lithium Hydroxide (LIH) plant in the UK. Currently there are no LIH plants in Europe, even though it is the principal form of lithium required by battery manufacturers, in particular those using the most popular Nickel-Manganese-Cobalt variety. At present ninety per cent of the world supply of LIH comes from China which processes not only its own natural sources but also those from other countries such as Australia and Chile.

TVL is a wholly owned subsidiary and currently the only asset of Alchemy Capital Investments Plc, which listed on the main market of the London Stock Exchange in October 2021. Half the shares are held by the chairman Paul Atherley, who has held senior executive positions in various mining companies such as Pensana and Berkeley Energia.

The need for lithium-ion battery production is well known. In Europe alone 33 Gigafactories have been announced, 3 of which are in the UK. While China currently produces 79 per cent of such batteries this is expected to reduce to 65 per cent by 2025, with Germany becoming the second largest producer at 11 per cent[1]. It is also known that outside China the largest sources of natural lithium are spodumene rock in Western Australia and the Congo and salty lakes in the Andes, mainly Chile. What is less well known is what happens in between. The spodumene crystals need to be dissociated from other minerals and a pure lithium compound isolated, generally lithium sulphate. The water taken from salty lakes needs to be evaporated and separated to leave lithium carbonate. In both cases the results need to be purified and converted to LIH.

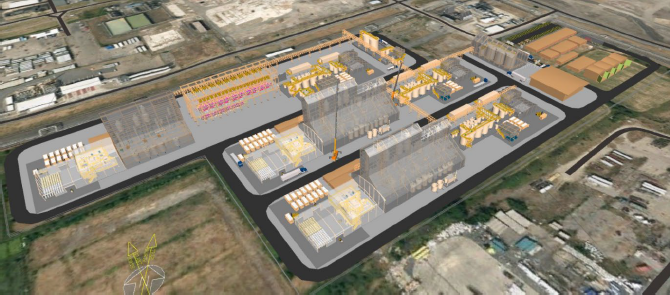

Image of the proposed processing facility (www.teesvalleylithium.co.uk)

TVL plans to produce 90,000 tonnes per year of battery grade LIH[2], and expect to satisfy about 15 per cent of European demand by the time the plant is completed in the late 20’s. The plant will process both lithium carbonate and lithium sulphate derived from spodumene, brine, mica (such as to be produced by British Lithium), or used batteries. There will be four production lines, one using the conventional method with sodium sulphate and three others using an electrochemical method with power from renewable sources. This is intended to minimise the carbon emission content. Nearly all the materials will be imported and exported.

Teesside was chosen not only because of the ease of import and export from its status as a freeport, but also because it can be located within the Wilton International Chemical Park, an established chemicals park that can provide all the needed services and infrastructure as well as being a market for the bi-products of the processing such as sodium sulphate and sulphuric acid. Certified renewable energy from offshore wind farms will allow it to claim that its products are low carbon. TVL have commissioned various studies on the chemical procedures and the financing. The underlying assumptions are that the long-term cost of lithium sulphate will be US$10,000 per tonne and that LIH can be sold at US$25,000 per tonne. With a thirty-year life and capital costs estimated at £1.49 bn there is a healthy rate of return.

With such a large mark-up the competition may be high. Why, for example, would the original producers in Australia or Chile not do this processing? No doubt they will, and already do to some extent, but one answer is that a vital property of the LIH is its purity. Achieving this involves multiple steps to clean the input material and crystallize the output. These are suitable for a chemical laboratory and not a mining operation. On the other hand TVL do not want to receive the raw rock, as is often sent by ship from Australia to China. The vast majority of this is waste, significantly increasing the carbon content of the eventual battery. TVL will expect the mining company to extract the lithium sulphate from the rock, a process it says can be done with a fairly simple acidification. Finally, the shelf life of LIH is short so there is an advantage in being close to the battery manufacturer.

TVL expects to receive permits in Q3 2022 and to have its first commercial production line running by Q1 2025. The demand for its product is clear and the emphasis on minimizing the carbon content admirable (although without a significant carbon price the commercial advantage may be small). The main risks are competition and the possibility of new developments in this very active area. Alchemy’s share price stands at 160p for a market capitalisation of £9.6 million.

[1] www.statista.com

[2] According to an Australian government publication, current world production is around 240,000 tonnes, but is currently growing at the rate of about 75,000 tonnes per year. LIH quantities should not be confused with pure lithium quantities.

{kind=link}

{kind=link}

{kind=link}

{kind=link}

{kind=link}