It is tempting when writing about tidal stream power to go into metaphor-land and question if it is a ‘drop in the ocean’ or whether it can “make a bigger splash” and become a key, or even a dominant part of the future energy mix, not just in the UK but also in other countries.

Atlantis Resources was founded more than a decade ago. It has been quoted on London’s AIM for three years now. According to the interim results for the six months to June 30 2017 revenue was £3.1million, losses before tax were £3.2m, cash at the bank was £6.7m and Atlantis raised £9.1m in new funding. The market capitalisation is currently £52.90m at today’s share price of 42p.

In October 2017, the company’s MeyGen flagship project (what Atlantis calls a world flagship tidal stream scheme) in the Pentland Firth offshore Scotland reached an installed capacity of just 6MW. It has produced a total of some 2.6 gigawatt-hours (GWh) of energy with rather over 800MWh dispatched during the month of September. All-in-all the company’s profile suggests it is still a functioning minnow rather than a group that is about to radically transform the world’s energy mix.

But appearances can be deceptive. The company is nothing if not ambitious. It says its core business is to develop, finance, construct and operate large scale renewable energy projects in the US, Europe. North America, Asia and emerging markets; and claims 1000MW of power projects in various stages of development. It believes it can leverage multi-million dollar partnerships with governments, utilities and corporations to create marine power schemes.

One example of this approach is Indonesia where Atlantis has signed a deal for Phase 1 of the 150 MW Nautilus tidal stream project in Lombok with SBS Energi Kelautan (SBSEK) the owners of the project. The agreement is an important step towards a firm order for 8 x 1.5MW Atlantis 1500 turbine systems. Tim Cornelius CEO of Atlantis said: “I am delighted that Phase 1 of Nautilus is moving ahead in earnest. ……This would represent our largest ever equipment order from Asia and with 100 x 1.5MW planned, the total project would equate to a multi- hundred million dollar supply contract for Atlantis”.

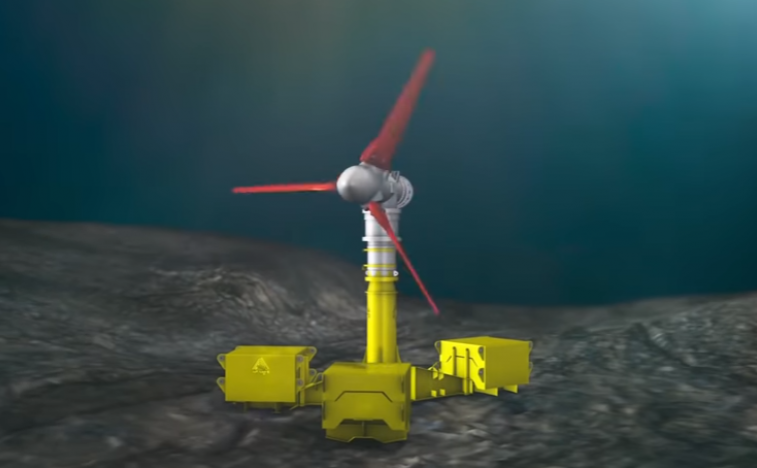

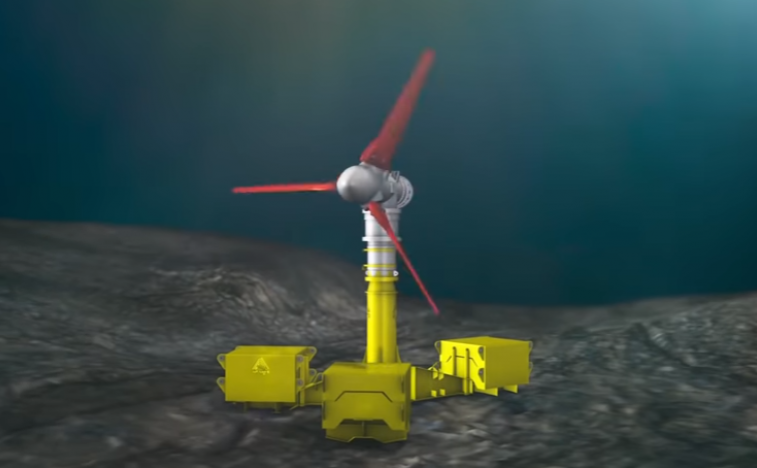

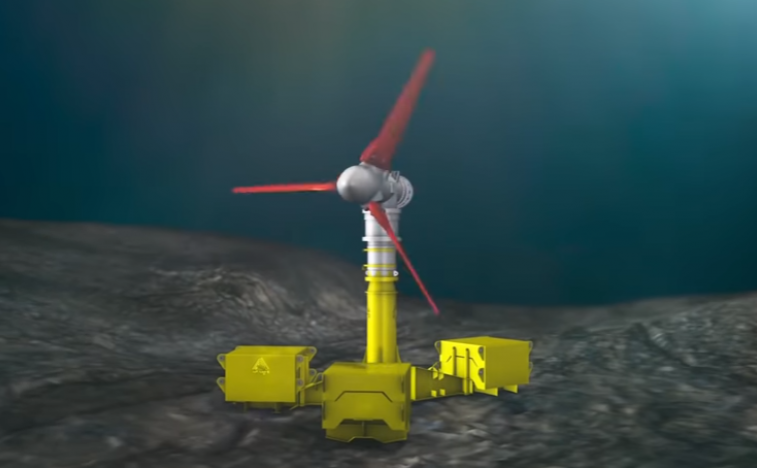

A tidal current turbine–part of Atlantis’s flagship MeyGen tidal stream project offshore Scotland, photo: www.atlantisresourcesltd.com

There are also examples closer to home, namely the above mentioned MeyGen project. But while the Indonesian project has been underwritten by a long term contract with a local utility, Meygen has been funded thus far by the UK government and EU money: in addition, MeyGen’s Phase 1A was completed with help from Scotland’s Renewable Energy Investment Fund (REIF).

Atlantis is now moving ahead with phase 1B of the project which is scheduled to double MeyGen’s capacity In January 2017 the European Commission awarded £17.3m (Euros 20.3m) in Horizon 2020 grant funding for Phase 1B. This money is in addition to the previously awarded Euros16.8m under the NER300 programme. Atlantis now wants to get on with Phase 1C of MeyGen which would add 80MW to the project’s generating capacity

This is proving to be a bit tricky because the funding is unlikel to be grant funding. In September the Department for Business, Energy and Industrial Strategy (BEIS) held a Contract for Difference (CfD) auction. This is the instrument the BEIS uses to support ‘less established renewable technologies’. There was great surprise when two of the three companies involved were awarded CfDs for £57.5 per MWh from an offshore wind farm. In 2015 offshore wind farms were given support amounting to £114 and £120 per MWh.

Atlantis submitted an application for a CfD of £300 per MWh and was unsuccessful. This is really the point. While offshore windfarms are considered early stage renewable energy projects, tidal marine power is thought to be even earlier stage with the necessary technologies not yet fully proven. The company’s share price fell from a 52-week high of 71pence to 31.50p, following news of the outcome of the auction.

But we have by no means reached the endgame. Although disappointed, the company said in September: “We intend to ask the UK Government to consider entering into bilateral negotiations with us for the award of a 15 year CfD contract.” The proposed strike price would be £150 per MWh..

Since the CFD auction, the share price has recovered somewhat to 42p. It has been estimated that some 29 terawatts of untapped power generation lie within tidal systems around the UK.. According to Atlantis, about a third of that, so far theoretical power, can be harnessed from the Pentland Firth. So there is still plenty to play for.